Brokerage Bonuses are extremely undervalued and can make 5k to 30k/yr for middle class households and cut off multiple years of work, with very little risk and with a very small time commitment.

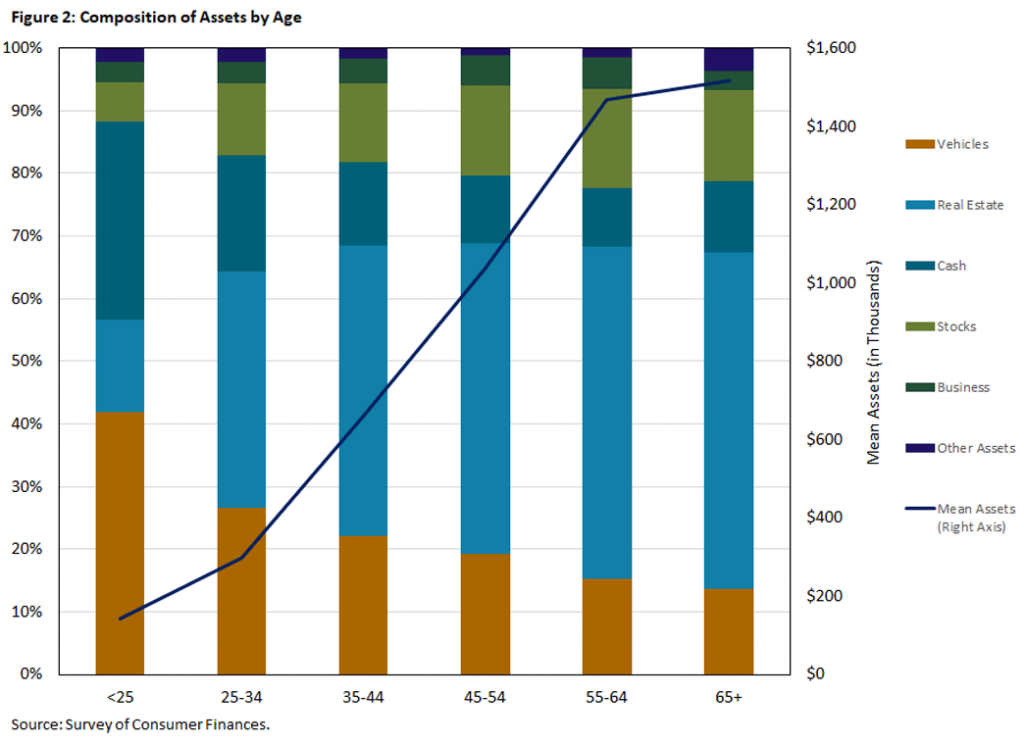

This figure from the Richmond Federal Reserve shows the average (mean?) households’ assets in 2023. Note that the amount of cash+stocks ranges from about 50k at 25-34 to about 400k at 55-64. (Incidentally, I’m puzzled that the value of vehicles for the 55-64 year old crowd appears to be over $200k).

If you’re going for early retirement or financial independence to reach a certain goal net worth, a .5% to 2% bonus on your portfolio will cut 2-6 years off a 30 year working/earning phase with a portfolio that earns real returns at 7%. At 5% real returns, it cuts off 3-8 years. Even with a very conservative .5% APY, you save 2 years of full time work for about 10 days of work. Of course, this assumes these bonuses will exist indefinitely, but for now, they are holding strong.

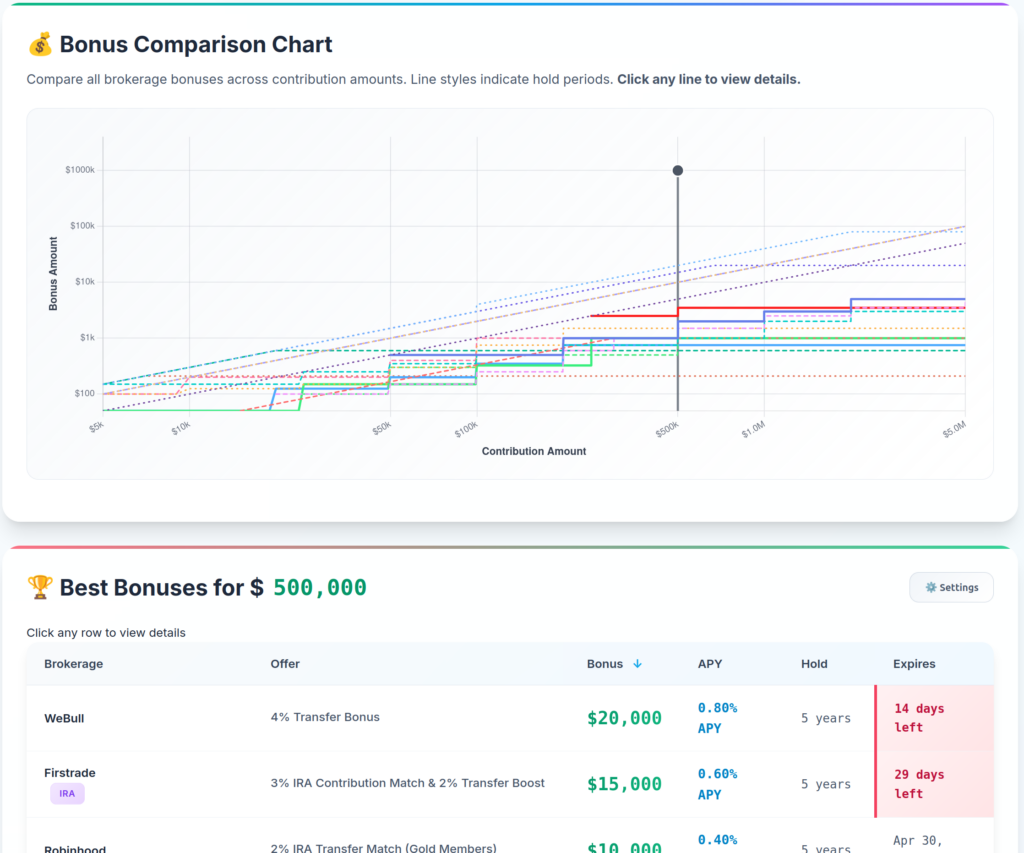

The best source of information for this is doctorofcredit.com‘s brokerage bonus page, though it’s a bit noisy and hard to track. So of course it became something for me to try out AI on.

I did 4 sessions of Claude Code to make brokerage.bonusprofessor.com, which allows you to see the highest APY and absolute bonus you can get by transferring your already invested stocks and ETFs from your current brokerage to the next one. With the 50k level, you can easily find 1-2% APY bonuses, which will bring in $500-1000/yr. At the 400k level, you can get 4-8k/yr. If you are in the Financial Independence or boglehead circles, you will probably balance relatively lighter on real estate ownership and heavier on stock returns, so portfolio values will be from 100k to 2M.

I would posit that 95% of the population doesn’t know about the bonus landscape, and the ones that have heard of it tend to think of it like credit card bonuses or bank deposit bonuses. The main objections to brokerage transfer are that it’s a pain, and it’s dangerous. If you use brokerages that are covered by SIPC up to 500k, which is the case for literally 100% of bonuses that I came across, the risk is minimal. The main pain is you might get your transfer messed up, rejected, or in the worst case, the brokerage will liquidate something because they don’t support it, triggering capital gains. This is relatively rare, and simple to minimize the risk of (don’t try to transfer US bonds or mutual funds or options unless you are certain they can be transferred).

I’ve done over 10 of these, and put the average time involved at 1 hour per brokerage. The worst offenders were CITI (3 hours) and MooMoo (5 hours). Most you just submit the form and wait. If you want to specify a partial transfer, this takes a little longer because you have to specify what you want, but not more than 10 minutes. You also need to set a calendar event for when the hold time is done if you want to transfer out, but it’s also fine just to stay at the brokerage if you like it.

Compare this to credit card bonuses or bank bonuses, which probably take a similar amount of time and probably more tracking (e.g. spend for credit cards). Credit card bonuses are probably worth 1k to 3k each at best, but the brokerages can easily top 10k.

It’s possible to get 2% APY, but I think it’s fairly easy to do 0.5% APY with any net worth. This would shave ~2-6 years off a 30 year work life if assuming 7% real returns. It also could be used to open up more freedom to invest/diversify into other areas including real estate, or some angel investing in things close to the heart, like longevity biotech in my case.